The nature of the main features of the organization. Addition of basic benefits - features and procedure Basic benefits after their addition, be insured

The main costs for accountingThey present an important and, in some respects, complex appearance. Regardless of the development of the OS (owned by a company or from production), it is important for the accountants of the organization to have a clear understanding of the rules and norms of the environment that apply to the OS itself. This article has this article about those that the Fahians should know in advance.

The outline of the main features of enterprise in 2017-2018: what has changed

I first ask the accountants of the enterprise to clearly understand the differences and similarities between the approaches to the development of OZ and the operations with them in the accounting and supply department of OZ.

Both in accounting and in accounting, in order for the company to respect the continued possession of its main function, the entity must meet the following criteria:

- The actual term of the victorious object lasts 12 months;

- the object is intended for sale to the state enterprise, and not for resale;

- the building asset brings economic benefits to the business;

Until 01/01/2016, the criteria for the primary value of the OS in the accounting department were avoided by the following: OS was considered to be in possession, with a value of over 40,000 rubles. Alez 01/01/2017 r. at paragraph 1 of Art. 256 and paragraph 1 of Art. 257 of the Tax Code of the Russian Federation was amended, apparently before any operating system began to recognize the method of subsumption as a minimum, which is worth 100,000 rubles per pound. In this case, the increased limit is expanded even if adopted from 01/01/2016 OS. For Bukhoblik, the value of the limit has not changed: the main thing that is depreciated is recognized as an asset to the owner for 40,000 rubles. In connection with which between the subsoil and the bagoblok, time differences are established that are subsumed.

The skin object of the OS should be applied to a small shock-absorbing group, as the weariness is deducted from spending over a long hour-long period.

The main change in the form of fixed assets, which was introduced in 2017, was a change in the codes of the Transgalno-Russian Classifier of Fixed Assets (OKOF), in connection with which the terms of depreciation of certain fixed assets changed, and certain types of fixed assets were transferred and to another depreciation group. The new standards will apply to healthcare facilities put into operation after 01/01/2017.

IMPORTANT! The object was put into operation before 01/01/2017 and after the new OKOF became operational, it was included in a different depreciation group, or the term of the corrugated depreciation, the depreciation rate changed there is no need to overinsure.

We learned about the nuances from the material.

The procedure for purchasing an OS from a company

If a company acquires (or retires) an OS, the job of accountants will ensure that the fact that the company owns the OS is correctly reflected, as well as the subsequent appearance of the OS in the accounting department.

The first thing to do in this context is to determine the primary quality of the OS object. It is important for him to know what makes up such virtuousness.

As follows from clause 8 of PBO 6/01, the primary responsibility is determined by the way of summing up all expenses that the company actually did in order to add the object and bring it to the stage, if it can be used for production. in, and itself:

- The price of a bath or the quality of life. If the operating system for the company is a counterparty, deductions can be confirmed using an additional act of acceptance and transfer, invoice, act of receipt, etc.

IMPORTANT! The price is included until the first sale without VAT. The maximum permissible limit is insured by the OS company, only if such an operating system is used by the company for activities not subject to the maximum permissible limit.

- The amount spent on the delivery of the object from the distributor (colossal hairdresser) to the company. For accounting purposes, proof of this part of the primary ownership of the OS is provided by a bill of lading or roadbill (if the company independently brought its OS).

- Find out how the company was interested in knowing, so that the object became attached to the victorious plant. To this group, costs include costs for installation, installation, etc.

- If the company imported the OS object from behind the border, then at the primary warehouse you can also collect the fee specified in the declaration. At this point, zocrema, the Federal Tax Service of the Russian Federation indicated on the sheet dated April 22, 2014 No. GD-4-3/7660@.

- Keep in mind that payment is necessary for the object to become a company of the manufacturer. Confirmations of such debits may simply require payment instructions regarding the payment of the mit.

- Whether there were any other expenses, it was necessary to recognize the company in connection with the OS accessories.

FUCK THE RESPECT! The core importance of the accounting system in the form of taxation lies in the fact that it allows you to insure in the first place the investment asset for the amount of loans that the company had to take as a means of adding such asset (clause 7 of PBO 15/2008, approved by order of the Ministry of Finance dated October 6, 2008 No. 107n ). In the subordinated form of the building there are no sales costs.

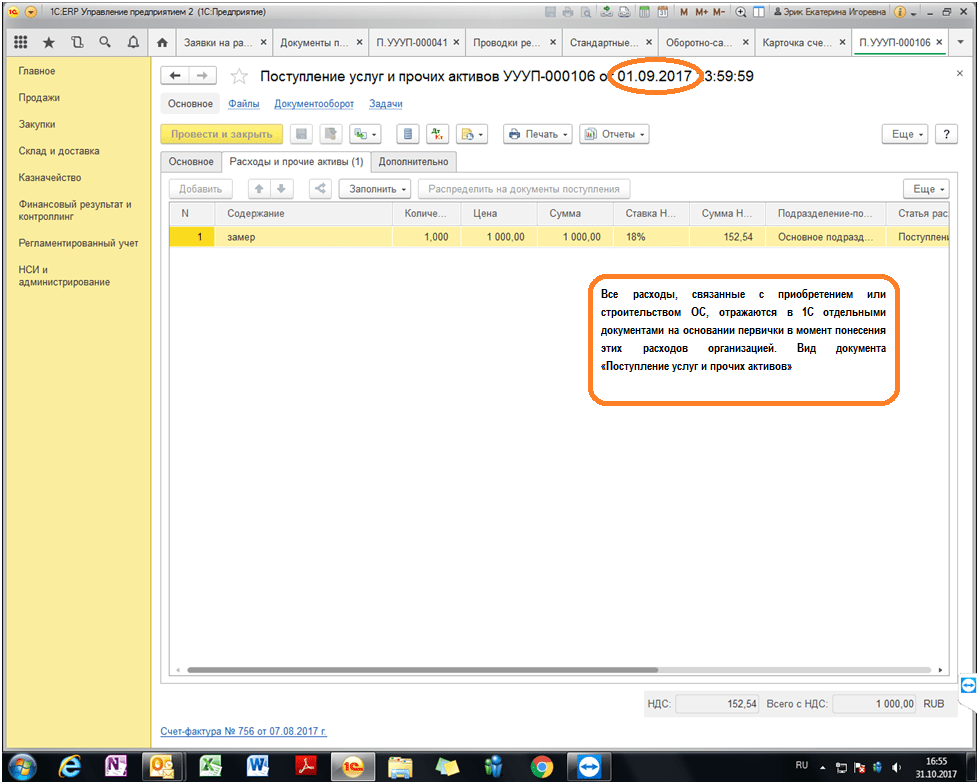

Butt molding of varosti OZ in the accounting department based on 1C ERP version 8.3 representations below:

After the fact that the company's supplier maintains the original value of the OS, such an object can be accepted for purchase. For which company you need to fill out a trace, then open it for a special purpose.

IMPORTANT! Companies should be aware that the OS must be registered with the authorities, this procedure is not applicable at the time of approval to the bank. Such a moment, in any case, occurs on the date when the primary ownership of the OS object is determined.

Depreciation and revaluation of fixed assets for a bookstore

The firm depreciates the OS over the course of an hour of operation, so that its wear and tear is gradually transferred to frame 02.

FUCK THE RESPECT! Depreciation in the form of OS should not be interrupted. The blame applies only to canned health care products longer than 3 months, as well as for health care products whose renewal may last longer than 12 months (paragraphs 17, 23 PBO 6/01).

It is important for the accountants to remember that certain categories of operating systems do not need to be amortized. Before them lie, for example, plots of land.

Also, the company has the right to re-evaluate its fixed assets, i.e., carry out a revaluation as a result of the value of the fixed assets, and the amount of previously charged depreciation. This follows from clause 15 of PBO 6/01. Such a re-evaluation may lead to the end of skin cancer. In this case, the results of revaluation (values of revaluation or discounting) can influence the financial results of the company, as well as increase/change the company’s additional capital.

Report on the re-evaluation of the OS. at statti .

Organization of an accounting department for the sale of OS

If the company plans to sell OZ, then the alcohol specialist has the task of correctly showing the fact of sale to the accounting authorities. What accounting heritage causes OZ sales?

1. On the date of sale (transfer of power rights to the new ruler), the selling company will show income. Such income is secured from the warehouse of others and accumulated in account 91 (for the loan).

IMPORTANT! Income is the net selling price, excluding VAT. However, for account 91, all income is immediately insured, after which the amount of MDV for the operating system is reflected in the debit of account 91 in correspondence with account 68.

2. Sales of operating systems are subject to the need to make excess profit from such operating systems and other companies spend.

Find out about the specifics of selling OS to a liquor store.

Part of the documentation of the sale of an OS to a company includes a memory trace of the transfer of the OS to the purchaser, which is recorded in an acceptance certificate.

It is important to remember during the hour the sale of unsold assets

In fact, problems often arise when a company plans to sell an unproduced new OS, for example, warehouses and booths. There is also a trace of remembering the peculiarity of the booze block.

In addition, income from the sale of such unproduced objects is also considered other income and is credited to the account 91 of the amount that the buyer paid for the object.

However, the fragments of shortcomings of the object have not yet been recognized by the company as an OS, and therefore cannot be formed in the first place. It's a matter of food that must be included before consumption.

IMPORTANT! How to indicate paragraphs on those. 11, 14.1, 16, 19 PBU 10/99, approved by the order of the Ministry of Finance of the Russian Federation dated 05/06/1999 No. 33n, in this situation other expenses (debit of account 91) of the company should include these expenses and how she has already suffered a connection with the OS (in fact, the date of sale of the property was determined), and, as is relevant, the subsequent sale was spent (for example, on the intermediary’s fee and others).

As if there is a sale of OZ, when selling an unexploited object, the income accrues (and is shown in the report) on the date when the ownership rights passed before the start.

Nuances of the purchaser transfer of OS to the statutory capital of LLC

If the company decided to transfer its assets to the statutory capital of another organization, remember that such transfer must be formalized by a separate deed. They can be folded either in a free form or with a different template, the OS-1 form. In this case, it is important that such an act reflects the excess value of the OS, as well as the value of the maximum permissible value, which the company will be required to pay in connection with the transfer of the OS as a contribution to the CC of another company.

Dali. The transferred OS is assessed by the participants of the receiving organization based on the size of the contribution made by such OS. It is important for the company to understand that participants evaluate the operating system for its value, which outweighs its regional value, the difference the company makes for its income (credit account 91 from correspondence with debit account 76 assigned to the region to the company's engagement with a third-party company for its contribution to the CC). In the last episode, since the shareholders assessed the OZ at a smaller size, it was indicated in the company’s accounting documents, it turns out that in fact the debt for the deposit in the CC was not repaid until the end. Therefore, the difference should be included in the warehouse of other expenses and written off to the debit of account 91.

To determine the depreciation on the OS, as well as the contributions from the CC, read.

Liquidation of OS from booze

Liquidation of the OS may be done in a similar way to a booze block.

First of all, the remainder of the income for the operating system that was lost was not taken away by the company, the company will have to show that it wasted only a little. Before the debit (which appears behind the debit of account 91), this type includes the following:

- too much versatility of the OS, which is liquidated;

- the amount of expenses for work (both authorities and third parties) that directly supported the liquidation of the OS;

- The value of the maximum permissible value, which the company managed to renew in connection with the liquidation of the OS.

Yaki postings fold up at vibutya object OS cm . V materials .

In other words, the traders responsible for the OS stock should not forget that as a result of liquidation, the company will take away new material reserves. They must be credited to account 10 (by debit) in correspondence with the increase in other income of the company (credit 91).

Read about how to restore and spend time to liquidate OS.

Pouches

The accounting aspect of the main features in 2017-2018 will continue to follow the same order as before. And accept the OS form as of the date of completion until ready for use. Every year, the sale of OS from a wine city is included in income, and the surplus value of OS is included in expenditure. Similar rules are being extended for sales of unproduced objects. In this case, it is important for accountants to remember: regardless of those in the accounting department, the vartisny criterion for recognizing an OS object has increased to 100,000 rubles, in the accounting department, it has not changed, as before, become 40,000 rub.

Based on the PBO "About the Main Assignments" (PBU 6/01), the main assemblies are not limited to those assigned to the company as a means for more than one purpose (for example, development, equipment, equipment, transport) or for rent (Leasing).

Thus, the varity of the lane with the term of service is greater than the lower river (regardless of the price) to be taken into account 01 "Basic Costs".

This rule is wrong. The main price does not cost more than 20,000 rubles. (without maximum permissible limits), then it can be purchased from the MPZ warehouse (clause 5 of PBO 6/01). In this case, organize additional control over the flow of such a main function for its preservation.

The company may set a lower limit on the availability of the main features that are written off after they are put into operation. You need to write about this to the regional accounting police.

Those who are otherwise careful to take care of the stock of basic features, since such minds are suddenly lost:

It is intended for the production and management needs of the company;

Mainly vikorystuvatimut for 12 months;

The company does not intend to oversell it;

Mayno can generate income.

A unit of the main features is an inventory object. Such an object can be:

Other objects (for example, a butt, a wardrobe, a car, a refrigerator, etc.);

A single complex of many objects that are mounted on a foundation or provide underground control (for example, a personal computer, which includes a system unit, a monitor, a keyboard, a mouse).

Subject to the Foreign Russian Classifier of Fixed Assets (Approvals of the State Standard of the Russian Federation dated 26 April 1994 N 359), the accounting department is informed of the following main features:

Sporudi,

Workers and power machines and equipment,

Variable and regulating devices and devices,

Calculation technology,

Transport facilities,

Tool,

Virobnichy and Gospodar's inventory and equipment,

Working, that breeding thinness is productive,

Bagatory plantings,

Internal roads and other related objects.

Capital investments for the complete cultivation of land;

Capital investments leased the main facilities;

Land plots and environmental projects.

Do not appear:

Items that serve less than 1 fate,

Items are sold below the limit established in the regional policy, and not more than 20,000 rubles,

For fishing,

Tools for purposeful purposes,

Special and branded clothes and clothes,

Bedding,

Timchasi sporedi,

Young animals, the last creatures,

Bagatory plantings in the gardens.

Addition of main facilities

The main assets are represented in the accounting department at the highest level.

The balance sheet shows the excess amount (primary value for the amount of depreciation charged for them).

Pochatkova vartіst of the main cost is the sum of actual costs for this addition and creation. Vaughn to lie down since the main purpose was taken away:

For pennies;

As a contribution to statutory capital;

Free.

Also, the main benefit can be created by the company itself.

Purchase of the main purpose

According to the rules of the accounting department, the primary value of the main sum received for money includes all company expenses associated with the purchase price, with the exception of the maximum allowance and other contributions that must be accounted for.

With such contributions:

The sum paid in advance of the contract to the buyer (seller), as well as for delivery and further examination of the object;

Amounts paid for information, consulting and intermediary services related to the addition of basic services;

Mita and mitni collections;

Taxes, which are not subject to payment, are paid to the state, but must be paid in connection with the accessions of the object of the main interests;

Other expenses are directly related to the equipment, equipment and preparation of the main facilities.

All transferred expenses are insured by the debit of section 08 “Investments in non-current assets”, subsection (depending on the type of purchased mine):

08-1 "Approaching the land plots";

08-2 "Approach to environmental objects";

08-4 "Attachment of the main facilities";

08-7 "Pridding for grown-up creatures."

If the company pays the PDV, then the amount of the contribution presented by the seller of the main value is not included, but the primary value is not included, but is charged to section 19 “Deposit for added value for added valuables”, sub-rate 1 “Deposit for added value for additional valuables” zasobiv".

After the main product has been prepared, it is taken before drying (on the shelf of the seller's invoice).

If the company does not pay the maximum allowance, then the amount of the contribution will increase the initial amount of the main fund and will not be accepted until the tax recovery.

The purchase of the main item is indicated by the following transactions:

Debit 08, subrack 1 (2, 4, 7), Credit 60 (71, 76 ...)

It was insured to spend on the purchase of the main property;

Debit 19-1 Credit 60 (71, 76...)

The maximum allowance is insured for the expenses associated with the purchase of the main cash (on the basis of the seller’s invoice);

Debit 60 (71, 76...) Credit 50 (51)

Pay the main payment and expenses associated with your purchase;

Debit 01 Credit 08, subrack 1 (2, 4, 7)

The object of the main features has been accepted to the accounting department;

Debit 68, subrahunok "Rozrahunki z PDV", Credit 19-1

The maximum permissible value for taxes associated with the purchase of the main cash is accepted before the subordinated insurance.

butt. In the chest of the famous fate, the enterprise has been added to the agreement. Yogo price became 118,000 rubles. (The maximum permissible limit is 18,000 rubles.) The cost of delivering the workbench to the company's workshop and installation was 23,600 rubles. (The maximum permissible limit is 3,600 rubles.) The Aktiva accountant is guilty of carrying out:

Accountant's work table

The balance of the business for the World River will indicate the primary value of the verstat in the amount of 120,000 rubles.

Contribution of the main contributions to the statutory capital

Since the company has taken the main benefit as a contribution to the statutory capital, it is necessary to hold it on the balance sheet for the share agreed between the principals.

In a joint stock partnership, the price of the main stock can be confirmed by an independent assessment. In case of a partnership with limited liability, it is turned over, since the main payment costs more than 20,000 rubles.

The transferring party is required to update and pay up to the budget before accepting the MDV for the main cost in proportion to its excess value. The party that receives it is responsible for accepting the maximum permissible value, and then can accept it before recovery (Clause 3 of Article 170 of the Tax Code of the Russian Federation).

butt. ZAT "Aktiv" (the founder) transferred ownership to the established company "Pasiv" as a contribution to the statutory capital. It is accepted and confirmed by the estimated value of 500,000 rubles. (without regulation of the maximum permissible limit). Zalishkova's balance sheet value of the assets of "Active" is set at 550,000 rubles. The maximum permissible value in the amount of 99,000 rubles falls on it. The cost of delivery to the owner was 11,800 rubles. (The maximum permissible limit is 1800 rubles). The accountant of "Passive" has completed the following activities:

Table 2 - Accountant's work

|

It is shown that "Aktiv" is involved in a deposit with the statutory capital |

||||

|

Accepted to the form of possession |

||||

|

Insured PDV with possession |

||||

|

Transport costs shown |

||||

|

Insured maximum permissible limits for transport tickets |

||||

|

Installation put into operation |

||||

|

Adopted before the MDV is revived. |

The balance sheet of "Passiv" for the starry river for the article "Basic Costs" has a value of 510,000 rubles. according to the depreciation insured for it.

Maintaining basic needs without costs

If the cats are taken free of charge, their value is determined at a market price similar to the price.

The transfer is free of charge and the amount given is over 500 krb. fenced between commercial organizations (Article 575 of the Central Committee of Ukraine).

In this way, the main functions of the organization can be terminated free of charge only by individuals, non-profit organizations, as well as state and municipal bodies.

The MDV amount for such a main sum, paid by the side that is transferred, will not be accepted until the tax recovery. There will be greater versatility.

The range of the main features, which can be taken away free of charge, is represented by the following:

Debit 08-4 Credit 98-2

The main benefits were taken away free of charge.

When you put the main features into operation, make a record:

Debit 01 Credit 08-4

The main features have been put into operation.

The supply of material assets, free of charge from another organization or individual, contributes to the income. A tax must be paid for the bags of the period when the bags were purchased.

It is important to establish values that are taken away by a company as an individual or an organization that has a share of the statutory capital of your business of at least 50%. In the event of such retrieval, the profits will not be deposited, only because they will not be transferred to third parties by extension on the day of retrieval.

butt. In the old days, enterprise took away technological ownership free of charge from the local self-government body. Its market value was 360,000 rubles. (including maximum permissible limits). The accountant of a business is responsible for carrying out:

Table 3 - The accountant of the enterprise is responsible for carrying out:

DEBIT 09 CREDIT 68 subrahunki "Rozrahunki for income tax"

72000 rub. (RUB 360,000 x 20%) - added to the taxable asset, charges for the property of the garage, included up to the taxable asset in the case of realized income.

Creation of the main feature by the company itself

The main payment can be made. There are two ways to wake up:

Contractor (when work is carried out by third-party organizations - contractors);

Gospodarsky (as the company conducts its activities independently).

In the accounting department, the primary responsibility for the main functions, generated in any of these ways, is the sum of all expenses for their upkeep and commissioning (expenses for the purchase of materials, equipment and installation of equipment, payment praci robotnikov, etc.).

After the work is completed, an act is drawn up for the assigned cost of living. In support of such an act, you must carry out the following:

Debit 08-3 Credit 60

The virtuousness of daily life is depicted;

Debit 19-1 Credit 60

The amount of maximum permissible value assigned to the invoice of the contracting organization is shown.

butt. In a mature family, business began in the everyday life of administrative work. Business activities are carried out in a consistent manner. The total amount of all work totaled 2,360,000 rubles. (The maximum permissible limit is 360,000 rubles.)

Table 4 - The accountant is responsible for completing the work (after execution of the act):

Under the government method, the firm carries out daily work independently (so as not to involve contractors). In this case, all expenses related to everyday life (production of everyday materials, depreciation of basic assets, which are used for everyday life, wages of labor workers, etc.), and also insure for children betom rakhunka 08.

In appearance it is depicted as follows:

Debit 08-3 Credit 10 (02, 70, 69...)

It is possible to spend money on everyday work, victorious by powerful forces.

The performance of construction and installation work for the smooth organization is subject to maximum allowance. With this amount of donation, collected during the Viconn’s work, it encourages the recovery of the mind, so that:

The object of virobnic significance was prompted;

The MDV amount was overinsurance to the budget.

Adding basic services for a penny fee is the most popular way of organizing. Such an object accounts for the sum of all extra pennies spent.

At the cob stage, it is important to correctly determine the type of purchased mine that meets the criteria for the main characteristics.

Added value for a fee may be included in the fixed assets warehouse, as:

- The object has been in use for a long time.

- The object will not survive like an MPZ.

- The asset cannot be sold at the earliest possible date, as it is associated with the product.

- Mainly plans to vikoristuvatime otrimannya profit.

- The limit is limited to the minimum established by the organization (no more than 40 thousand rubles for a bakery, for a sub-serve the limit increases to 100 thousand rubles).

Important! The job of the accountant is to establish the significance of the criteria and correctly identify the purchased value.

If the criteria are not met, the object can be recognized as either a material or a product without depreciation warranties.

What documents are required to document the transaction?

The object is purchased from the buyer for a fee that is agreed upon in advance. The price of the asset is specified in the delivery and purchase and sale agreement. At the time of transfer of the mine value to the buyer, an act of acceptance and transfer is formed. As a rule, the parties formulate the deed form using the standard form:

The object is purchased from the buyer for a fee that is agreed upon in advance. The price of the asset is specified in the delivery and purchase and sale agreement. At the time of transfer of the mine value to the buyer, an act of acceptance and transfer is formed. As a rule, the parties formulate the deed form using the standard form:

- - For single objects that are durable;

- – inclusive for sporades that are transmitted;

- – where a number of assets of identical type are purchased for a fee.

If you accept the possession of a warehouse without vikorist as an OS, then it will be vikorist.

The transfer deed is filled by both parties with the main document, on the basis of which the object can be considered as the main document.

The form of such expenses appears on the document base:

- invoices;

- Acts of service, work.

The purchase of OS includes expenses for payment of the cost of the contract, as well as other expenses related to transport, installation and others.

The object starts to turn off.

Reserve OS-1

The transfer act is drawn up on the skin side. Form OS-1 contains a number of sections that are left behind, whether the object was previously in operation or not. For the new main assets, there is no need to fill out the first section; here, only the data on the assets that the company had was collected - the period of recovery, cob wart.

The other section is filled in the copy of the party that receives, data is provided on the day of acceptance to the form - vartіst, the term of the correspondent with the arrangement of the indicators of the first section.

The OS-1 act form is signed by both parties.

Butt stock act of capture and transfer to the main person:

Accounting appearance

The value of the product was purchased and tested for the price, which is called . This information includes the purchase price specified in the supply agreement, and the associated expenses of the enterprise from the additional payment for the asset.

Pochatkovu vartіst when purchasing is molded:

- The amount that the seller is overinsurance upon purchase is indicated in the contract (the maximum permissible value is established, if an invoice is given, the amount of insurance will be included in the subordinate maximum permissible activity);

- tax on the added property at the purchase price, since the main purpose is not intended for the activity subject to VAT;

- payment for transport services;

- wasted, associated with folding and bringing the asset to a form suitable for use;

- Mita and collect, as they are;

- Additional expenses are spent, for example, on refurbishment, when a new device is sent to purchase an OS until a different location.

At the initial stage of acquiring the main fund, all expenses incurred for the purchased object are collected for a fee. The collection is collected according to the debit of account 08 - this is a special additional intermediate account, which allows you to fill up the accounts of all expenses and cover the total amount of the purchased main cash with the settlement of all expenses.

Important! In fact, the video cards at the front door form the corn varity according to the debit of 08 rakhunki.

The account is prepared with accounting entries under debit 08 for correspondence with the following accounts:

- 60 – withdrawal for immediate payment under the contract for the asset;

- 60 – spent on third-party services (transport, installation, commissioning);

- 70, 69 - salary and insurance coverage for personnel who are engaged in the work of the organization’s health workers;

- 71 - when the object buys a new device that is being recharged.

After recording all expenses for the purchase of an object that needs to be purchased, a single transaction is completed - the amount of all expenses is transferred from credit 08 to debit 01 ( wiring D01 K08), where the main charge and will be counted until it is necessary to write it off or transfer it to another person.

Carrying out at the entrance for an OS fee

Posting table:

|

Operation |

Debit |

Credit |

| The postal owner's price for the object is shown in investments in the asset | ||

| The services of third-party organizations were insured (transportation, warehouse and handling robots) | ||

| The salary of the official workers of the enterprise, which is engaged in bringing the object to the required level, is insured by deposits | ||

| Included up to the deposit charged to the insurance fee | ||

| The maximum permissible value for all expenses associated with the purchase of the main property is shown | ||

| Acquisition asset as the main contribution for the sum of all expenses |

butt

Mind the butt:

The main asset was purchased - a photo printer for 118,000 (MPE = 18,000).

It was delivered by a transport company for 1180 (maximum allowance = 180).

Wiring for this butt:

|

Suma |

Operation | Debit |

Credit |

| The price stated in the contract was insured, without the settlement of the deposit. | |||

| The maximum permissible value is shown at the price of the postal owner and is depicted separately | |||

| Insured services of a transport company | |||

| Submissions for transport services were seen | |||

| Reinsurance of unprepared payment to the postal owner for the main payment under the contract | |||

| Reinsurance of payment to the transport company | |||

| Delivery of a photo printer upon arrival as the main requirement | |||

| MPE direct to outlet |

Features of the acquisition of an asset that is in operation

As a company, then, by the way, the accounting form of such an asset is in no way different from that declared for objects that have not been in operation. Postings from the form of earlier vikoristnyh OSs themselves.

Single shift - that's it possibility of shortness of term of corysous vikoristan at that hour, having worked for a long time with the former ruler. The operating time can be determined from the transfer deed, which is drawn up between the parties at the time of purchase. Once a standard act form is generated, this information is provided in the first section. The term is expressed in months and is taken from the SPI that can be set for the object, depending on the OS classification.

Important! It is possible to change the term of the korisnogo vykoristannya for the adopted main purpose, which is in operation, If the seller is an organization or individual entrepreneur. Such individuals may be able to confirm with a document the real term of the operating system.

Depreciation on an asset that is owned by the company, in which case it will be necessary to adjust to the terms of the changed term of operation.

It is possible that the object that is in the victorious market, having drawn up its SPI, then the seller has the whole vision for a new term for classification. These SPIs can be determined independently based on safety precautions.

Peculiarities of acceptance in a physical individual

Since the main purpose is to buy from a citizen without the approval of an individual entrepreneur, then the rights are regulated by a bilateral purchase and sale agreement concluded between the buyer company and the seller - an individual. For consumption, the agreement is supplemented by a transfer deed.

Since the main purpose is to buy from a citizen without the approval of an individual entrepreneur, then the rights are regulated by a bilateral purchase and sale agreement concluded between the buyer company and the seller - an individual. For consumption, the agreement is supplemented by a transfer deed.

It is also permissible to replace the agreement with an act with one document - a purchasing act.

Buhoblik has the main benefit falls in primary order on the stand of the wiring indicated above.

If the OS is in use, you cannot change the OS. The term must be reinstated according to the classification.

More donations, then the main benefit of paying an individual for purchases from her is:

- there is no need to reduce PDF,

- there is no need to obtain health insurance;

- It is impossible to see and determine the maximum permissible limit.

Oblik under the simplified tax system income minus expenses

Companies in a simplified mode are eligible for the purchased main sum turn on your devices only after putting it into operation. As for intact objects, it is a rule that they will be acquired only after the document on the retention of rights to the new one has been withdrawn.

Important! The procedure for payment of expenses for the purchase of operating systems must be established at the moment the law is committed: before the transition to the SSP or at the time of transition to this mode.

What main payment was purchased on the simplified tax system:

- in the first quarter - the varity is attributed to the consumption of equal parts of the skin from four quarters of the flow rock;

- in another quarter there are three equal parts in the skin of three quarters of flow rock;

- in the third quarter - two equal parts in each of the two quarters of the flow rock, which were lost;

- in the fourth quarter - with all my money.

What OS was purchased before the simplified tax system:

- previously the GSN was stagnant - until the withdrawal, the surplus vartisny display is turned on for the remaining day before the beginning of the stasis of the SSP for the tax data;

- Previously, the UTII was stagnant - in the same way, the excess amount of money was taken before the withdrawal, and then after the data to the booze block.

Withdrawal for the main payment, purchases before the simplified tax system, is debited from the account with the following rules:

- SPI up to 3 l. - almost equal parts for the first river of work;

- SPI 3 to 15 l. - the first rock of the robot - 50% of the share (12.5% quarterly), the other rock - 30% (7.5% per quarter), the third rock - 20% (5% quarterly);

- SPI higher 15 l. - The first 10 years have 10% health care (2.5% each quarter).

Zalik MDV

As a rule, the price of the object being purchased includes the maximum allowance. The company will not be able to accept you until recovery. In some cases, the contribution must also be made to the deposited asset.

As a rule, the price of the object being purchased includes the maximum allowance. The company will not be able to accept you until recovery. In some cases, the contribution must also be made to the deposited asset.

When the MDV extends the flow:

- It is planned that the main goal will be to participate in operations with the support of MPE;

- Є rakhunok-invoice – її is presented by the postal owner, and the s/f can clearly see the contribution from the assigned rates;

- Three days have not passed since the date of purchase.

Butt: The receipt of the main amount falls on the 1st quarter of 2018; you can apply for a renewal of the maximum allowance no later than the 1st quarter of 2021.

If the asset requires installation work, then the maximum allowance can be submitted no earlier than the quarter in which the equipment was accepted before installation on frame 07. If it does not require major installation, then the repair can be declared no earlier than the quarter in which the main function was assigned Iksovana for debit 08.

Butt: the asset was purchased in the 1st quarter of 2018, the price of the postal owner is reflected in the debit of the account 08 in the 1st quarter of 2018. Also, the maximum permissible value at the price of the postal owner can be calculated in the 1st quarter, shown in the declaration for that period.

If the maximum permissible limit cannot be determined:

- There is no rakhunka-texture;

- As a result, the object will be victorious in operations that do not comply with the MDV.

Such a contribution must be shown in the warehouse deposit in the asset - turn it on before debit 08.

There may be a situation where the OS becomes stuck in both compliant and non-compliant operations. Then you need to see the part of the contribution that falls on the offense of the type of operation. In this case, part of the maximum permissible value will be deducted (attributable to the subordinated operations, and part will be included in the part of the main cost).

Korisne video

The order of the main considerations when purchasing - information for beginners:

Purchasing the main asset, the organization must take stock of the asset that will result in all expenses incurred for additional accounting entries. The maximum permissible value from deductions can be seen before it is released, if the counterparty has issued an invoice, and the main payment is planned to be used for operations based on the invoice and payment of the maximum permissible value.

Main features- Part of the lane, which is used as a means of working with the production of products, the company works either as a dedicated service or to manage the organization during a period that exceeds 12 months or emergency operations This cycle lasts 12 months.

Inventory object- This is one of the main features. The inventory of the main features is an object with all the attachments and attachments or a complete structural and reinforcement object, intended for the creation of new independent functions, or a complex of structurally articulated objects, which is We aim at it and the purposes for victorian singing work.

Capital contributions- Spend enterprises on creation, increasing the size and power of government, on adding basic features intended for the trivial growth in government activity.

Depreciation of main assets- Repayment of the property of the main facilities.

Repair of main facilities- Correction of damage and replacement of worn parts of the object. In-line repair – replacement or renewal of replacement parts; medium repair - partial disassembly of an object and renewal of a worn-out object; major repairs - external disassembly from the replacement of worn parts or their upgrades.

Main features of the enterprise

Main features of the enterprise- Part of the mine, which vikorist is rich in yakity during the production of products, vikonanny works either for the provision of services or for administrative needs of the organization over a period that exceeds 12 months.

The main features of the enterprise include the following types:- were;

- sporudi;

- work and power machines and equipment;

- vibrational and regulating devices;

- computing technology;

- transport facilities;

- tool;

- vintage and gospodar's inventory and equipment;

- productive and breeding thinness;

- rich plantings and other fixed assets.

Lines of korisnogo vikoristanny- During this period, during any period of time, any component of the main features of the enterprise may generate income for the organization or serve for further purposes of its activity. During operation, the main equipment of the plant is subject to wear and tear. There is a moral and physical deterioration. Moral deterioration- The waste of booths, spores, machines, automatic machines and other possessions of their wealth as a result of scientific and technological progress and increased productivity. Physical wear It appears as a result of active installation work and as a result of the influx of natural forces (metal corrosion).

One of the accounting areas of the main features of the enterprise is the inventory item with all the devices and accessories or other structurally reinforced items. The main expenses of the enterprise are accepted to the accounting department for the first time, that is, for the amount of actual expenses for the addition, development and preparation of the main assets. The organization has the right to re-evaluate the objects of its main functions for its financial value no more than once per year.

Depreciation of the main assets of the enterprise

The cost of assets of the main activities of the enterprise is extinguished in the form of increased depreciation (transfer of the assets of the main activities of the company, the production of goods, the supply of services). If the primary responsibility is to collect the amount of depreciation costs during the service life of this object, then there will be an excess amount.

At this time, depreciation of the main assets of the enterprise can be done in one of the following ways: linear, modified surplus, for the sum of the numbers of losses, the line of the cash flow and write-offs of the reserve in proportion to the total amount of products (rob it).

The actual amount of depreciation and amortization insurance is calculated as follows:- with the linear method, proceeding from the primary value of the object and the rate of depreciation, calculated in accordance with the line of material of the object;

- in the method of changing the surplus resulting from the surplus value of the object to the beginning of the star rock and the rate of depreciation, adjusted in accordance with the term of the solid rock of the object;

- with the method of writing off the vartosti for the sum of the numbers of rocks coming from the primary vartosti of the object and the river relationship, in the number book there are a number of rocks that will be lost until the end of the term of service of the object, and in the sign - the sum of the numbers of rocks in terms of the object's service.

For other objects of the main features of the enterprise, which are excluded from contracts for granting and free of charge, housing stock, objects of modern improvement, forestry and road management, productive thinness, rich plantings, as well as additional materials (books, brochures) And then again) depreciation does not increase.

Updating the objects of the main features of the enterprise can take the form of simple or expanded development. A simple installation looks like replacing or overhauling the main components. Expanded - in the form of new everyday life, expanded production, reconstruction and technical refurbishment, as well as modernization. When simply created, cats do not change their sweet and sour characteristics. In case of expansion, a change in quantity is required, which means switching to the capacity, based on the basic principles of accepting a new replacement. If you spend money on modernization and reconstruction of objects after completion of these works, you can increase the quality of the objects.

There are various reasons for the changes in the main aspects of business: moral and physical wear and tear, or the fact that they are taken into account; sales (sales); free transfer; transfer as a contribution of statutory capital to other organizations; liquidation in case of accidents, natural disasters and other emergency situations. The totality of the main activities of the enterprise, which are constantly being used for commercial needs, is written off from the balance sheet.

In organizations it is possible to identify the active and passive part of the main functions of business. The active part infuses the process, moves them in the process of production and maintains control over the progress of production (machines, equipment, transport vehicles, etc.), and the passive part creates a mind-friendly functioning of the active part (the івлі, срUDі, інгора и ін.).

The effectiveness of the development of the main features of business

The most important indicator that characterizes the main features of a business is its subsidiary. Who will have the varsity displays? For example, the output of products in Vartisnomu is 1 rub. average quality of basic features; Vikoristannaya obladnannya per kіlkistu. Therefore, it is necessary to separate the preparation, installation, operation of the plan and actual operation of possession; vikoristannya control over the hour, and also separate the calendar, schedule, planned and actual hours; removal (release) of products from one area. - Relation of the average level of the main features of the enterprise to the average number of workers at the greatest change. The technical state of the main features of the enterprise is characterized by the following factors: renewal; vibutya; growth; wear and tear; availability of basic benefits, and the costs of their replacement.

Organizations are given the right to lease, temporarily free and the main features of the enterprise, which are not subject to rent.

When to separate the trace:- I'll pay for the rent- Rent out certain objects to the lessee in a timely manner;

- long-term lease- transfer to the lessee for the balance of the whole complex of the main features of the enterprise with the right of further redemption;

- leasing, or a financial lease - an addition by the lessor to the agreement of the lease of adjacent objects, either with or without the right to purchase. In this case, the landlord places them on his balance sheet, or the landlord transfers the object to the landlord’s balance sheet.

Rent is the basis of the contract of the mine, which transfers the terminology of the mine, which means the transfer of the landlord to the landlord for a fee. You can hire both Rukhoma and Nonrukhoma Main. In accordance with the law, the agreement provides for sovereign registration.

There are two parties involved in the lease agreement:

- landlord - the owner of the property who rents him out (as the landlord can act in the same way as individuals, authorized by law, or the landlord to give the property for rent);

- orendar - the possessor of the lane, who is victorious for his own purposes, obviously before the recognition of the lane or with the minds of the agreement.

The most extensive method of establishing a rental payment is a flat payment calculated based on the price of each mine that is being rented, or on the basis of the warehouse parts. Payments must be made periodically according to the terms established in the agreement. However, a one-time payment is possible. The leaseholder is the owner of the production and income taken from the inheritance of the leased mine.

Okremy view of the orendnyh vydnosin - building lane for hire. Enterprises can be transferred to the main hiring periodically, whenever there is a temporary need for unfulfilled objects; Rentals are available on a permanent basis. Maino, transferred behind the lease agreement, is called vikorystovuetsya leaseholder for entrepreneurial activity; When renting out the mine, you will be required to use it for temporary purposes. The terms of the rental agreement are non-obligatory, so the rental agreement is limited to a period of up to one term. Therefore, it is generally not allowed to build a lane under a sublease rental agreement.

Leasing is a type of lease, which contains elements of positional transactions, which makes it similar to a loan. It also includes components of external trade and investment activities. The Law “On Leasing” interprets it as a type of investment activity from the acquisition of a mine and the transfer of it under a leasing agreement to individuals or legal entities for the installation of lines, for a fee and in accordance with the minds secured by the agreement with the law vikupu maina lizingooderzhuvachem.

The main advantage of leasing over a traditional lease lies in the fact that in this case three parties take a central role:

- lessor (tenant) - a physical or legal person who acquires power and transfers it at the right time to the leasing owner for a fee and on the terms of the agreement;

- leasing owner (lessor) - a physical or legal person who accepts money from the owner in accordance with the leasing agreement;

- seller (post owner) - a physical or legal person who sells to the lessor the property that is the subject of the leasing agreement.

In the process of carrying out leasing activities, the lessor is subject to expenses associated with the additions and transfer of the mine to the leasing owner, as well as expenses due to the need for the creation of minds for the normal development of the mine transferred to the lease .

Classification and assessment of the main features

Subject to clause 4 of PBO 6/01 “The scope of the main assets”, the warehouse of the main assets of the enterprise insures assets such as:

- vykoristyvayutsya in the production of products for the production of work and services or for management needs;

- subscribe for more than 12 months;

- further bring income to the organization;

- will not be available for sale next time.

The main features include: working and power machines and equipment, vibration and control equipment and devices, computing equipment, transport equipment, tools, manufacturing and government equipment and equipment, working and, productive and breeding thinness, rich plantings and other basic get it.

The main ones also include capital investments in the final cultivation of land (drainage, demolition and other reclamation works) and in the lease of the main facilities.

Capital investments in rich plantings, complete cultivation of land are included in the stock of basic assets in the amount of investments that are required for the areas put into operation, regardless of the completion of the entire complex of work.

The warehouse of the main features is insured by the authorities of the organization of land plots, environmental objects (water, water and other natural resources).

If there are many parts of one object, so to speak, the skin part is insured as an independent inventory object.

To organize the environment and ensure control over the preservation of the basic properties of the skin object, the basic properties (inventory object), regardless of whether it is in use, in stock or on conservation, must be assigned when They will be released to the accounting department with the corresponding inventory number. The inventory number assigned to the object of the main features is saved throughout the entire period of its use by this organization.

Inventory numbers of the main assets written off from the accounting entity are not assigned to newly acquired assets for a period of 5 years after the completion of the write-off.

The subject area of the main assets is maintained by the accounting service on inventory cards for the area of the main assets (form OS-6). The inventory card is assigned to each inventory item. Inventory cards can be grouped in the card index of the entire Russian classifier of fixed assets, and among divisions, subdivisions, classes and subclasses - at the place of operation (structural subdivisions) or organization).

Replenishment of inventory cards (inventory book) is carried out on the basis of the act (invoice) of acquisition and transfer of main assets (form OS-1), technical passports and other documents for the addition, disposal, transfer and write-off of objects of main assets iv. In the inventory cards (inventory book) there will be provided basic data on the subject of the main features: the term of the currency, the method of charging depreciation, the type of depreciation charging ( what the place is), individual characteristics of the object.

Inventory cards, as a rule, are stored in one example and are distributed to the accounting service.

For the main purposes of the lease, in order to create an off-balance sheet view of the lessor's assets, it is also recommended to open inventory cards.

Acceptance of objects of the main assets to the accounting department takes place on the basis of a certified organization document (invoice) for the acquisition and transfer of the main assets, acceptance to the accounting department of the same type can be completed who, however, are of new virtuosity and accepted to form instantly.

The main funds are accepted to the accounting department at the time of their acquisition, investment and preparation, contribution by the principals to the account of their investments to the statutory (stocked) capital, deduction from the grant agreement and other assets for the primary management.

The total cost of the main services added for a fee (closed to the operation) is the amount of actual expenditures of the organization for the addition, preparation and preparation, in addition to the tax paid and other compensation contributions.

The objective of the main features is carried out in rubles, and when adding objects of the main features, the value of which is denominated in foreign currency, the assessment is also carried out in rubles by reorganizing the foreign currency at the rate of the Central Bank of Russia ii, what is current on the date of acceptance to the accounting department of the organization objects from the right of authority, sovereignty, operational management and lease agreement.

The validity of the main principles in which they are accepted in the accounting department does not subject to change, except for the differences established by the legislation of the Russian Federation and the provisions of the accounting department “The scope of the main principles” (PBO No. 6/01).

Changes in the initial quality of the main facilities are allowed in cases of extraction, refurbishment, reconstruction and partial liquidation of the main facilities or carrying out work of a capital nature, as well as through a reassessment of the main features.

If a business decides to re-evaluate its core competencies, it will have to work hard. Revaluation can be either an increase in the value of the main features (revaluation) or a change (discount).

As a result of the additional assessment, the primary value of the main assets increases and account 01 “Basic capital” is debited from the correspondence with a credit to account 83 “Additional capital”. At the same time, the amount of accumulated depreciation for overvalued fixed assets increases: debit line 83 “Additional capital” and credit line 02 “Depreciation of fixed assets”.

For the accounts of the valuation of the main assets, the primary value of the main assets is changed and the posting is made: debit to the "Additional capital" account and credit to the "Fundamental capital" account and the amount of charged depreciation for the transfer is immediately changed. Other main assets: debit to account 02 “Depreciation of main assets” and credit to account 83 "Additional capital".

If the additional capital does not rise to cover the amount of the markdown, that part of the markdown that exceeds the amount of the previous additional assessments is written off as a balance sheet and is credited to account 84 “Non-divided profits (Uncovered surplus).” Who has the following transactions: debit account 84, credit account 01 and debit account 02, credit account 84.

As a result of the revaluation of the main assets for level 01, the new value of the main assets is insured.

An increase (change) in the primary value of the main capabilities is due to the additional capital of the organization.

Before the reconstruction of existing enterprises, it is necessary to renovate the main workshops and facilities of the main, primary and service purposes, as a rule, without expanding the obvious activities of the main purpose, associated with improved production and production movements of its technical and economic level, with the understanding of the reach of scientific- Technological progress is due to a complex project for the reconstruction of the enterprise, which has led to an increase in labor force, an increase in production capacity and a change in the product range, most importantly without an increase in the number of workers per hour. Improving their minds is the purpose of protecting too much middle ground.

Before the additional development or technical refurbishment of existing enterprises, a set of steps must be taken to advance the technical and economic level of the surrounding production plants, workshops and plots based on the introduction of advanced equipment and technologies, furs reduction and automation of production, modernization and replacement of outdated and physically worn-out factory equipment and related services.

In case of spending the organization, development of capital investments, after completion of extraction, acquisition, reconstruction of the main facilities, or after completion of work that may be of a capital nature, write off debit the account of basic benefits.

At the same time, the amount of capital expenditures received before the completion of the investment increases the amount of additional capital that has been lost from the organization (with the exception of depreciation).

Methods for adding the main features and the order of their presentation in the accounting department

Bathroom for a fee

p align="justify"> The main way to obtain the main funds for the enterprise is long-term investments (capital investments) in the main funds. The appearance of such investments is maintained on the calculation balance sheet 08 “Investments in non-current assets” under the following sub-accounts and under each object of everyday life and the addition of basic assets for a fee. The number of assets of the main assets put into operation on the basis of assets for capturing completed assets is written off from account 08 “Investments in non-current assets” to the debit of account 01 “Fundamental assets”.

With this method of adding the main personnel for a fee, based on low regulatory documents, the amount of actual expenditures of the organization on the addition, development and preparation of these basic assets is determined.

Pursuing the main efforts to navigate the path of new life and life from the expansion of existing enterprises.

Before the new operation, the complex of objects of the main, auxiliary and service functions of the newly created enterprises, as well as branches and other production plants, which will be reused after putting into operation and on an independent balance.

If the daily life of the enterprise is planned to continue in the future, then the next day will be until the next day until all projected efforts for the further development of the enterprise (sporudi) are put into operation.

With the expansion of regular business, the increase in labor force may be achieved in a shorter period of time and for less pet expenses in equal amounts of similar labor in the path of the new everyday worker This is due to the immediate advances in the technical level and the reduction in the technical and economic indicators of enterprises in general.

The existence of objects can be achieved in a number of ways and in the government's own way.

In the case of the contract method, the responsibility for all work is reported to section 08 "Investments in non-current assets" of subsection 4 "Addition of main assets" for the sections of contracting and design organizations. Why should you get insurance and spend money on the equipment that requires installation? Under the government's method of work, the wages of workers who take part from the work are allocated to non-budgetary funds, collection of wasted materials and low-value equipment, wear and tear of tools, time-consuming devices and appliances; The cost of ownership, which requires installation, expenditure on cleaning the equipment, and other expenditures. The procedure for reporting operations from the daily life of objects in the accounting department using contractual and government methods is given in Table. 4.1.

The order of displaying the appearance of the object's main features Table 4.1|

Box no. rakhunki |

sum, rub. |

Pidstava (document) |

||||||

|

I. With the contract method, the creation of an object of virtual significance |

||||||||

|

The advance payment of the design organization for the preparation of design and cost documentation has been re-insuranced to the extent of 100% return |

Agreement, bank statement |

|||||||

|

Accepted design and cost documentation by the design organization |

Rakhunok-faktura and act of viconnyh robіt |

|||||||

|

Fee for added vartіst behind the invoice of the design organization (18%) |

Rakhunok-texture |

|||||||

|

Accepted before payment of the contractors' fee for construction and installation work |

Rakhunok-texture |

|||||||

|

Tax on added value (18%) |

Rakhunok-texture |

|||||||

|

Payment to the contractor has been made |

Whisper note for a jar |

|||||||

|

Acceptance before payment of the postal owner's rakhunya from the bathroom equipment for installation at the time of the object's activity |

Rakhunok-invoice, invoice |

|||||||

|

Maximum permissible limit for rakhunkom na pridbannya obladnannya (18%) |

Rakhunok-texture |

|||||||

|

Payments to customers for possessions have been made |

Whisper note for a jar |

|||||||

|

Transferred to installation |

Certificate of delivery and installation |

|||||||

|

Zrobleno zalik with budget with maximum permissible limit |

Act on putting into operation, transfer of assets to the subdivision |

|||||||

|

Commissioning of the facility |

Act on putting the facility into operation |

|||||||

II. Under the ruler's method of creating an object of military significance

|

The advance payment of the design organization for the preparation of design and cost documentation for the construction of a living cabin was re-insuranced by 100% |

Agreement, bank statement |

||||

|

The design and cost documentation for the living quarters has been accepted by the design organization |

|||||

|

Maximum permissible value per invoice from the design organization (18%) |

Rakhunok-faktura, act of viconny robіt |

||||

|

The salaries of the workers who took part in the living quarters have been increased |

Rozrakhunkovo-payment information |

||||

|

Tax on personal income has been reduced |

Rozrakhunkovo-payment information |

||||

|

Salaries paid to health workers |

Rozrakhunkovo-payment information |

||||

|

Narahuvannya until: 1) social insurance fund (4%) |

Dovidka-rozrakhunok |

||||

|

2) pension fund (28%) |

Dovidka-rozrakhunok |

||||

|

3) medical insurance fund (3.6%) |

Dovidka-rozrakhunok |

||||

|

Written off materials for the living quarters |

Material expenses |

||||

|

MPE from written-off materials (18%) |

Accounting document |

||||

|

Built for installation |

Certificate of delivery and installation |

||||

|

Maximum permissible limits for the building and installation of equipment |

|||||

|

Putting the housing unit into operation and securing it to the warehouse of the main equipment |

Certificate of commissioning |

||||

|

The maximum permissible value was written off for the purpose of financing capital investments |

Certificate of commissioning |

Thus, the first priority in the wake of an object of military significance was in a consistent manner, accumulated 33 thousand. rub., And a living room - 39,560 rubles.

The business, in addition to the creation of basic equipment, can, under a purchase and sale agreement, purchase basic equipment from the finished product, as well as motor transport equipment, equipment that does not require installation, calculation of technical no way.

The amount of expenditures for the addition of other objects of basic services is insured under subsection 08-4 “Addition of objects of basic services.” The procedure for such representation in the accounting area is reviewed in the application of the enterprise under the purchase and sale agreement in the organization of trade of a vintage car for commercial purposes: car ownership - 35,400 rubles, including maximum allowance (1 8%) - 5400 rub. The costs associated with additional charges (delivery) were 1180 rubles, including the maximum allowance of 180 rubles.

The representation of operations on the accounting sections will be as follows:- debit rack 08/4, credit rack 60 - the amount of the added vantage is consistent with the invoice, without VAT - 30,000 rubles;

- rakhunka debit 19, rakhunka credit 60 - maximum permissible value for the main benefits that were found - 5400 rubles;

- debit rakhunku 08/4, credit rakhunku 60 - the sum of the deductions associated with the accessory of a vintage car, without the maximum allowance - 1000 rubles;

- rakhunka debit 19, rakhunka credit 60 - maximum permissible value for expenses for the vantazhivka accessory - 180 rubles;

- rakhunka debit 08/4, rakhunka credit 68 - tax collected for motor transport services - 6000 krb. (RUB 30,000 * 20%);

- debit rakhunku 01, credit rakhunku 08/4 - put into operation the main facility for actual expenses for the bathroom

37,000 rub. (30,000 rub. + 1,000 rub. + 6,000 rub.); - rakhunka debit 60, rakhunka credit 51 - paid for the main expenses and expenses for the bathroom - 36,580 rubles.

(RUB 35,400 + RUB 1,180); - rakhunka debit 68, rakhunka credit 51 - tax paid for motor transport services - 6000 krb.;

- debit rakhunka 68, credit rakhunka 19 - deposited for expenses from the budget of the amount paid for capital investments at the time of acceptance of a vintage car - 5580 rubles.

(5400 rub. + 180 rub.).

Supervision of the mini agreement

Under the contract, either a legal or physical person undertakes to transfer one product to the other party in exchange for another (Clause 1, Article 567 of the Central Committee of Ukraine). In this case, the skin side plays the role of the seller, and the role of the buyer. If the contract does not specify the transfer of the right of ownership, then the right of ownership of the goods will be transferred at the moment the parties sign the contract (Article 570 of the Central Committee of Ukraine). Since the first party relinquishes the main interests behind the contract, then until the moment of transfer of the right of authority (increasing the quality of the goods in place of the main rights taken away), this main interest is covered by the off-balance sheet account 002 "Commodity material assets accepted for special preservation." After the transfer of ownership, the ownership of the main assets is ensured in a manner similar to the purchase and sale agreement.

Extended to clause 3.5 of PBO No. 6/01, the primary value of the main benefits added in exchange for another mine, in addition to penny money, is recognized by the value of the main thing that is exchanged, for which it was in Shown in the balance sheet.

To reflect in the accounting field the main features of the vikoristan, the following output data: the enterprise under the contract acquires the object of the main features of the finished product for the mine that is transferred (manufactured products, goods, service), the property of which becomes 60,000 rubles. (without regulation of the maximum permissible limit). The valuation agreed upon by the parties to the barter agreement is RUB 94,400. (The maximum permissible limit is 14,400 rubles). In this case, the primary value of the object's main assets on the balance sheet is 100,000 rubles, and the depreciation charge is 30 thousand. rub., Apparently the excess (actual) vartіst for the accounting department deposited 70,000 rubles.

In this manner, on the other hand, this brings about the main advantages: 1. If the main features are met on the date of transfer of ownership of the property, the following will be exchanged:- for the balance sheet value of the lane, which is vibuable without the maximum permissible limit:

rakhunka debit 08, rakhunka credit 90/1 - 60 thousand. rub. (from paragraph 26 of the Methodical Accounting Notes on the Main Features... “on the date of transfer of ownership of the property that is being exchanged, the capital deposit account is debited from the correspondence with the credit account for the implementation"); - for the amount of maximum allowance - 18%:

debit rakhunka 19, credit rakhunka 90/1 - 12,400 rubles. (70000 x 18%). (Methodically, from the accounting department of the main principles, the rules for the representation in the accounting department of the main principles that come with the contract are established, and in this case, there are any recommendations for how to convert them into to the accounting department the sum of the input maximum permissible value indicated in the initial documents of the postal owner. tax legislation from the debit of the account on May 19, the amount of the maximum allowance amount is shown in full, assigned to the initial documents of the postal owner, which, by analogy, can be used for Methodical insertions from the accounting area of the main features of the main features of the part of the acquisition of the main benefits of the amount of the maximum allowance amount. may be displayed in correspondence with rack 90/3); - when put into operation:

debit rack 01, credit rack 08 - 60,000 rub.

- on the decommissioned lane that is being vibrated, for your own benefit:

debit rack 90/2, credit rack 41, 43 ... - 60,000 rubles;

debit 90/3, credit rakhunka 68 - 10800 rub. (MPE of charges arising from the amount of proceeds from the accounting department, which amounts to 60,000 rubles * 18%);

rakhunka debit 90/2, rakhunka credit 80-1800 rub.

- rakhunka debit 68, rakhunka credit 19 - 12,600 rubles.

- for the varity of the main duty that vibuva, without maximum permissible limits:

debit rakhunka 10 (41 ...), credit rakhunka 91 - 70,000 rubles; - for the amount of maximum allowance:

debit rakhunka 19, credit rakhunka 91 - 10800 rub.

- to write off the main sum for the first time:

debit rack 91, credit rack 01 - 100,000 rubles; - to write off previously accumulated depreciation:

debit rack 02, credit rack 91 - 30,000 rubles; - for the amount of maximum permissible value, due before payment to the budget:

rakhunka debit 91, rakhunka credit 68 - 12,600 rubles. (The PDV amount was calculated from the proceeds from the accounting department, which amounted to 70,000 rubles.) - to reveal the financial result of the mini agreement:

rakhunka debit 99, rakhunka credit 91 - 1800 rub. (Trace of the mother is respectful that the acceptance of this sum of money from the change in the financial result by means of submission of official regulatory documents has not been transferred.)

Free pick up

Subject to clause 3.4 of PBO No. 6/01, the primary value of the main features withdrawn by the organization under the grant agreement and in other types of free withdrawal is recognized as their market value on the date of purchase.

Expenditures from the delivery of designated objects of the main benefits, withdrawn from the contract of grant and other forms of free deduction, are insured as expenses of a capital nature and are set by the organizations supporting the increase in the initial value of the object. The allocated expenses are collected on the accounts in the form of capital deposits in correspondence with the accounts in the form of capital investments. In case of withdrawal of motor transport services by enterprises, the free payment for the addition of motor transport services is not subject to insurance.

Opributkuvannya of the basics of a reposition, Otrimannikh for a free time, get off the accounting region for a loan of Rakhunk 98 "Home the Maybutnih periodiv" Subrakhunki 2 "non -payment" at the bunks of the blessing of the non -console with the non -conveying activation. In the world, depreciation is accounted for (debit to account 20 “Basic production”, credit to account 02 “Depreciation of main assets”), income from future periods is included until post-realization income, part of the free withdrawal of main assets. Same with PBO - 9/99. This amount increases from the deposited profits (debit of the account 98/2, credit of the account 91). The introduction of the main features into operation is carried out in the following order: debit rack 01, credit rack 08. Subject to tax legislation, the receiving party is required to pay a tax on profits (24%), upon which correspondence I will be: debit 99 "Profits and earnings ", credit 68 "Rozrakhunki with taxes and fees."

Div. also:In the accounting department, a little more than 40,000 rubles can be borrowed from the inventory warehouse. As of 1 June 2016, the limit for the payment of basic benefits to the subordinated fund has increased from 40,000 rubles to 100,000 rubles. The main assets put into operation from 1 June 2016 are subject to a new limit of 100,000 rubles (Federal Law dated 8 June 2015 No. 150-FZ).

One of the main features is the inventory object:

- non-ferrous object (for example, butt, safe);

- A single complex of many objects that are mounted on a single foundation and provide behind-the-scenes control (for example, a computer, which includes a system unit, a monitor, a keyboard, a mouse).

For the main purposes, you are responsible for increasing depreciation. How necessary it is to work, marvel at section 02 “Depreciation of basic assets.”

Adding and putting into operation the main features

If your organization has added its main assets, you are responsible for keeping them on the balance sheet at the first rate. Pochatkova vartіst is the sum of actual expenses for the provision of basic services.

The acquisition of the object of the main features is shown in the debit of section 08 “Investments in non-current assets”:

DEBIT 08 CREDIT 60 (75-1, 76, 98-2, …)

- Acquisition of the object's main features.

DEBIT 01 CREDIT 08

Purchase of basic assets

If your organization added money for the fee (under the purchase and sale agreement or delivery), its primary value is the amount of all expenses associated with this purchase.

Such vitrates, for example, can buti:

- the amount paid to the seller in accordance with the contract;

- amount paid for delivery and installation;

- amounts paid for information and consulting services in connection with the addition of this facility to its main services;

- Mita ta zbori;

- taxes, which are not deductible, are paid to the state, which are paid in connection with the accessions of the object of the main interests;

- Deposits for loans and positions taken away to add the object of the main features, such as an investment asset;

- Other expenses are directly related to the addition of the main services.

Spend on the addition of basic assets and you are responsible for debiting account 08 “Investments in non-current assets” (without tax on added investment):

DEBIT 08 CREDIT 60 (76, …)